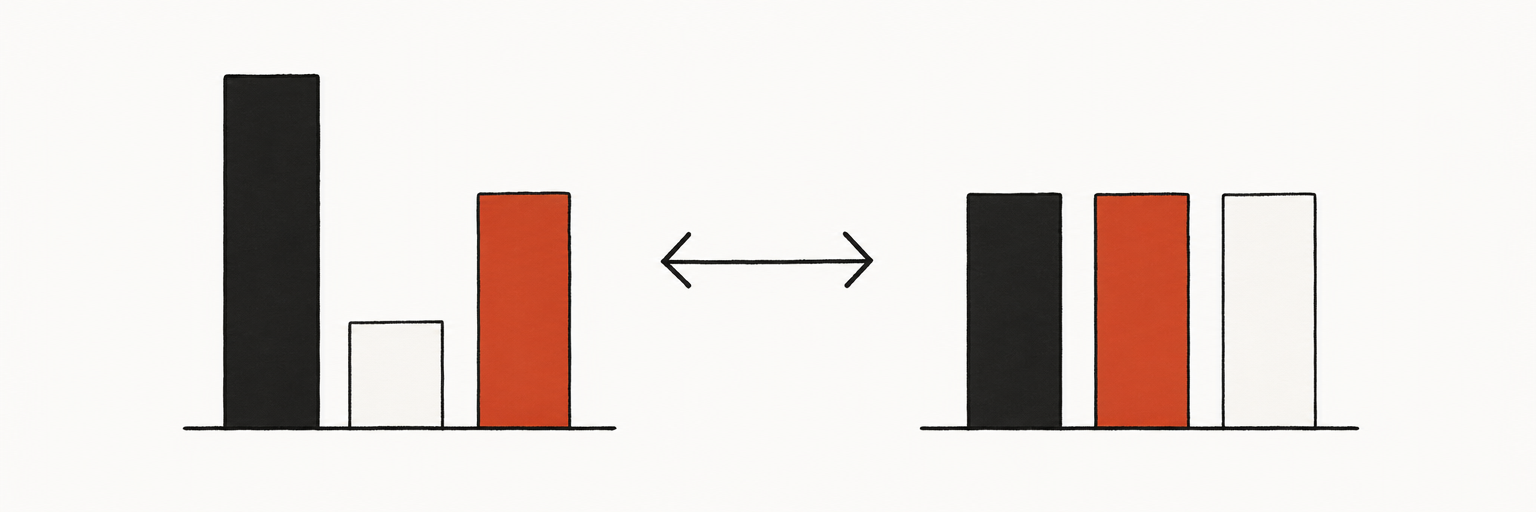

When you invest, you set a target allocation — a planned mix of assets like 80% stocks and 20% bonds. Over time, the market moves those percentages around. Stocks might grow to 87% of your portfolio while bonds drift to 13%. Your portfolio now carries more risk than you intended. Rebalancing corrects this: you sell enough of the outperforming asset and buy enough of the underperforming one to return to the original split.

How to rebalance: the three methods

Calendar-based: You rebalance on a set schedule — typically once a year. On a specific date, you check your allocation, identify the drift from your targets, and make the trades needed to correct it. This is straightforward and predictable.

Threshold-based: You rebalance whenever any asset class drifts more than a set percentage from its target — commonly 5 percentage points. If your stock target is 80% and stocks grow to 86%, you sell stocks and buy bonds to return to 80/20. This requires monitoring but avoids unnecessary trades when drift is minor.

Hybrid: You check on a calendar basis (annually or semi-annually) but only rebalance if drift exceeds a threshold. This is the approach Vanguard research has found most practical for individual investors.

How often is often enough?

Vanguard’s research compared rebalancing frequencies and found that annual rebalancing produces a risk-adjusted benefit equivalent to approximately 51 basis points (0.51% per year) compared to never rebalancing, and that this advantage disappears or reverses with very frequent rebalancing (monthly or daily) due to trading costs and tax drag.

For most investors: once per year is optimal. More frequent rebalancing adds cost without meaningfully improving outcomes.

| Frequency | Risk control | Cost/tax drag | Recommended? |

|---|---|---|---|

| Monthly | Tight | High | No |

| Quarterly | Good | Moderate | Rarely necessary |

| Annually | Good enough | Low | Yes — for most investors |

| Every 2+ years | Looser | Very low | Only for very stable portfolios |

What to actually do

-

Check your current allocation. Log in to your brokerage or retirement account. Look at the current percentage of each asset class: US stocks, international stocks, bonds, cash.

-

Compare to your targets. How far has each category drifted from your intended allocation?

-

Calculate the trades. To rebalance, determine how much of the overweight asset to sell and how much of the underweight asset to buy. Most brokerage platforms show this automatically in portfolio analysis tools.

-

Execute in tax-advantaged accounts first. Selling in a 401(k) or IRA doesn’t trigger capital gains taxes. In taxable accounts, selling appreciated assets creates a tax bill. Rebalance in tax-advantaged accounts first, then use new contributions to rebalance taxable accounts by directing them to underweight positions.

-

Use new contributions to rebalance passively. If you contribute regularly, direct new money to whichever asset class is below its target. Over time this reduces the need to sell anything, eliminating taxable events.

When a 5% threshold makes sense

If you’re actively monitoring your portfolio and want to avoid letting drift get large, a 5-percentage-point threshold is a widely used guideline. An 80/20 target portfolio would trigger a rebalance when stocks reach 85% or bonds reach 25%. This prevents large risk drift without triggering constant trades.

After rebalancing

Update your records. Note the date, the allocation before and after, and any trades made. Review your target allocation itself: if your timeline or risk tolerance has changed, adjust the targets before the next rebalancing cycle. The goal is not to return to an old allocation mechanically, but to maintain a deliberate allocation that matches your current situation.